When it comes to Mohammad Sanusi Barkindo, OPEC’s secretary general, it isn’t just what he says that counts, it’s the way he says it.

Barkindo gave a fascinating speech on Tuesday at the International Petroleum Week conference in London. It was fascinating chiefly because it seemed, if not entirely divorced from reality, then at least sleeping in separate beds.

The speech began on a decidedly defensive note, as Barkindo recounted the skepticism with which OPEC’s agreement to cut supply was met late last year. OPEC doesn’t have an exemplary record when it comes to abiding by such agreements, so high levels of compliance exhibited in January were apparently a slap in the face for naysayers.

Yet, as my colleague Julian Lee points out, such high compliance largely reflected OPEC kingpin Saudi Arabia bearing a disproportionate share of the burden, which looks unsustainable.

More telling was how Barkindo described the agreement: a “timely intervention” by OPEC and others “taken to address the prevailing market realities.”

In fact, dealing with market reality was what drove the original decision by Saudi Arabia — and, by extension, OPEC — not to intervene back in November 2014. Saudi Arabia could see then that propping up oil prices would simply mean ceding more market share to surging U.S. shale production and encouraging existential threats like electric vehicles, so the kingdom let rip. In contrast, the latest deal is an admission that letting the market decide things was inflicting too much pain on OPEC economies and not enough on U.S. producers.

For all the talk of markets, OPEC’s mindset hews more mercantile. There were plenty of clues in Barkindo’s language; phrases like “accord,” “declaration,” and “shuttle diplomacy” are more redolent of foreign policy than trading. The “historic feat” he hailed represented OPEC’s attempt to fight the market, not address it.

Where OPEC and the Market Sleep

Separate Beds

OPEC’s fundamental problem is that many of its members are unable to deal with the inherent cyclicality of the oil market. A true cartel would dominate oil production and have both a cushion of spare capacity and seamless coordination to iron out fluctuations in supply and demand. OPEC has none of these things. Indeed, Barkindo hails from Nigeria, a member country whose own production peaked more than a decade ago and is so beset by problems it was exempted from November’s agreement.

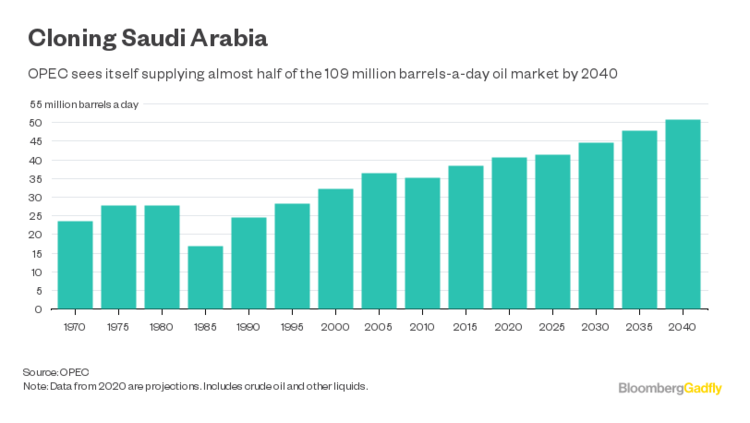

This makes a mockery of the forecasts Barkindo laid out in London. OPEC expects global oil demand to keep growing through 2040, by which time it will account for 46 percent of supply, up from about 40 percent now. That equates to an extra 12 million barrels a day from OPEC over the next 25 years, equivalent to another Saudi Arabia.

Barkindo is echoing, if less stridently, the sort of message OPEC officials used to deliver before the crash of 2008. In 2007, for example, OPEC was predicting oil demand of almost 118 million barrels a day by 2030, with the organization supplying almost 60 million of those. The numbers have come down, but the vision is the same: Oil demand will only go up and OPEC’s share will rise inexorably back to the glory days of the 1970s.

It is difficult to believe consuming countries will take OPEC at its word — after all, it was the organization’s inability to foresee and prepare for China’s boom in demand that led to triple-digit oil prices, which in turn touched off the shale boom and accelerated efforts to develop alternative energy sources.

Barkindo’s speech didn’t even acknowledge the impact of shale production. OPEC’s thinking is that the drop-off in investment over the past two years will lead inevitably to shortages and price spikes; Barkindo even hinted darkly at what might happen if a third year of lower investment transpires.

Yet the one place investment won’t drop again this year is in the U.S. Based on guidance given with quarterly earnings, Citigroup expects U.S. E&P companies’ spending to jump by 25 to 30 percent this year, according to a report published on Tuesday.

Unlike OPEC, the latter are actually dealing with “prevailing market realities.” Shale’s shorter (and shortening) investment timetables allow production to be curbed or raised much faster than in traditional fields. Operators also have access to the world’s biggest (and, seemingly, most forgiving) capital markets to cushion the blow of lower prices. Plus, liquid oil futures markets — which began in the 1980s in reaction to OPEC’s controlling impulses — give producers the ability to hedge their cash flows, enabling them to keep drilling.

Indeed, as energy economist Phil Verleger wrote in a report published this weekend, the glut of oil inventories OPEC aims to eradicate reflects the market at work, as excess barrels are bought by traders able to lock in profits by selling them forward. This inventory, maintained by market forces, is the market’s cushion now, keeping prices remarkably stable, not OPEC’s nebulous spare capacity.

Perhaps that is why Barkindo couldn’t resist a jab at “excessive speculation” toward the end of his speech on Tuesday. It is, after all, far more comforting to live in a world where your declarations are what really count.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Recommended for you