Some realistic comparisons with Norway

Both the Editor and I wrote in last month's Energy about the ongoing decline on the UK Continental Shelf (UKCS), particularly in relation to production and exploration.

Both the Editor and I wrote in last month's Energy about the ongoing decline on the UK Continental Shelf (UKCS), particularly in relation to production and exploration.

I do not want to start 2014 on a pessimistic note but I believe it is a good time to take a longer term view of what is happening on the UK Continental Shelf (UKCS).

It may come as a surprise to you but the fastest growing part of our energy industry in the UK at the present time is coal and not renewables.

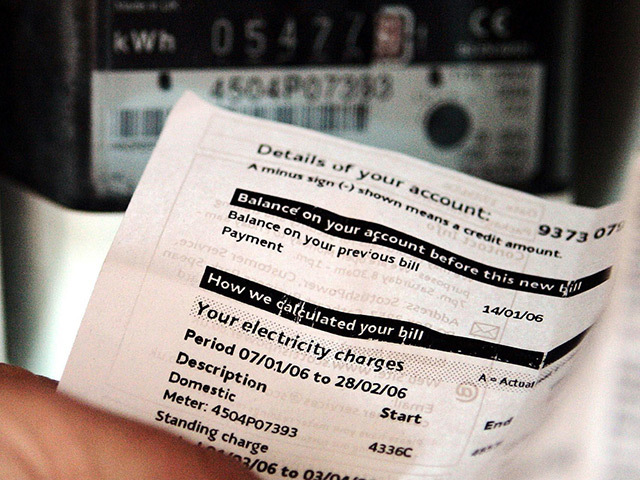

Most of the big six energy companies have announced annual gas and electricity price increases of about 10%, which have been met by understandable outrage.

Jan Minx and nine other academics have calculated the average carbon footprints of people living in every local authority area in the UK, including the 32 in Scotland. There is no space here to discuss the methodology but it seems to be very thorough and academically accepted.

These are challenging times for the oil industry, not least on the UK Continental Shelf (UKCS). The latest official statistics show UK oil production down 11% on last year and gas down 18%.

I've avoided getting involved to date in the arguments about future oil revenues if Scotland votes for independence next year and am still reluctant to do so.

There is enormous pressure in many countries to make illegal or undisclosed payments in order to win exploration licences, writes Tony Mackay.

A few years ago I did a study on oil prices for Christine Lagarde, then the French finance minister and now the head of the International Monetary Fund, writes Tony Mackay.

The European Union is going through a difficult period, mainly because of the economic recession.

The Scottish and UK economies have gone through a very difficult period since the financial crisis first hit in 2008. We have had nearly five years of little or no economic growth.

There have been a surprising number of reports in recent weeks on future government revenues from UK oil and gas production. The authors include the UK Treasury and Office for Budget Responsibility (OBR), the Scottish Government, Oil & Gas UK and academics from Glasgow University.

Mergers and acquisitions (M&A) in the oil and gas industry have attracted a lot of publicity in recent weeks. Various bodies have produced reports on the number and value, which appear to have reached record levels in some respects.

There has been a lot of good news from the North Sea oil and gas industry over the last few weeks, notably the announcement of over £5billion investments in the Mariner and Western Isles oilfields.

The last few weeks have seen an avalanche of energy policy announcements from both the UK and Scottish Governments. Some have been contradictory, notably from the Coalition in which Liberal Democrat and Conservative energy ministers seem to have very different views.

I was pleased to hear that the UK Government has agreed to investigate claims by a whistle blower that domestic gas prices are been rigged by traders in some of the companies involved.

There is huge and growing interest in unconventionals these days, particularly shale gas and oil. Moreover, there's an unconventional gas conference being staged in Aberdeen late this month.

Economic forecasting can be difficult but I like to think I have a good track record. I have produced hundreds of feasibility studies and market research reports, most of which have been reasonably accurate, although there have been a few that were not.

I have spent most of the last four months working in the South Pacific - in Fiji, Papua New Guinea (PNG) and a few other countries. Someone asked me if I would like to undertake a study on improving energy security in the region and after a few seconds hesitation I agreed. It has been a very enjoyable change from working in Scotland.

I worked in Norway for a year and am a frequent business visitor there. I took a sabbatical year from Aberdeen University to work at a research institute in Oslo, where with an old friend Terje Lind I wrote a book on Norwegian Oil Policies.

We probably all have hobbies or special interests. My elder daughter often berates me for the amount of time in my life I have spent watching football, either live or on television. Sadly, that must add up to years' despite my being an Inverness Caley Thistle and Scotland supporter.

I am currently in the South Pacific on a project intended to raise renewable energy output in the region.

Offshore accounted for about 32% of total world oil output in 2011 and some 24% of gas production. Both shares have increased slowly over the past decade.

I have read many reports on the UKCS decommissioning market over the last decade, as many other people in the industry must also have done. All have proved to be wildly inaccurate in relation to both the size and timing of the market, which has been very much smaller than predicted.

The Economy, Energy and Tourism Committee of the Scottish Parliament have asked me to submit evidence to their current inquiry into the Scottish Government's renewable energy targets.