The Spring Budget included the announcement of the formation of an expert panel to consider the impact of the North Sea tax regime on late life asset transactions, and promised the publication of a discussion paper to inform the panel’s remit. The discussion paper provides some insight into HM Treasury’s current thinking in this area and presents the industry with an opportunity to respond and get involved with the discussion.

Energy Jobline and Airswift have recently released the first edition of the Global Energy Talent Index (GETI), a market-leading report that investigates industry trends such as salaries and benefits, sector mobilization and hiring changes.

With the launch of the first Global Energy Talent Index, Sam Cross, senior vice president North America at Airswift, the global workforce solutions provider for the energy, process and infrastructure sectors, argues that to capitalise on the Trump administration’s energy ambitions, North American firms need to better understand the talent they want to recruit.

Over the last year or so there has been increased activity in mergers and asset transactions in the oil and gas sector. This certainly includes the UK Continental Shelf. With respect to asset transactions, in the immediate aftermath of the oil price collapse, there was little activity. Both potential sellers and buyers had to assess the effects of the price fall on the value of assets. Cost reductions and valuation of their effects were a priority. Also, there was great uncertainty regarding future price behaviour which made agreement valuations more difficult.

SSE have become the latest energy provider to raise prices for domestic customers, their announcement of a 14.9% hike in electricity bills coming less than a week after E.On’s own 8.8% rise to dual-fuel bills. Their news now means that all but one member — British Gas — of the Big Six have raised prices for the spring, yet aside from all requiring their customers to pay more for energy, they have something else in common.

It is fair to say that the UK is already world-leading in some aspects of nuclear power, like regulation, decommissioning and fusion research. The nuclear industrial strategy offers an opportunity to build on these foundations and return the UK to the top table internationally.

Few could have predicted the sequence of events triggered by former Prime Minister David Cameron, when in February 2016 he made his announcement on the steps of Downing Street that the Brexit referendum would indeed take place. Irrespective of the way people then voted on June 23rd 2016, very few would have wagered that the FTSE 100 index of leading shares would now be at a record high and that the UK would be one of the fastest growing economies in the developed world.

Recent comments on the job opportunities offered by onshore decommissioning activities have left me perplexed and dismayed. I can see no basis for them and they come from people who you would expect to know better. They include Jenny Marra, Labour MSP for North East Scotland, and trade unionists. Are they deliberately avoiding the facts in the hope of a self fulfilling prophecy – that there will be a jobs bonanza?

So what are the facts? The following is extracted from Scottish Enterprise’s Oil and Gas Decommissioning Plan (2016), which has been taken from Oil and Gas UK publications. As can clearly be seen the onshore spend is only a small fraction of the overall decommissioning expenditure - around 1-2%.

Though there are a number of legal obstacles in the way, it looks almost certain that there will be a second referendum on Scottish independence towards the end of 2018 or into early 2019. Brexit has fundamentally changed the context of the vote, and the UK can no longer present itself as the stable and secure option in the way that it could in 2014. That said, the arguments for independence are in many ways weaker now than they were then.

The oil and gas sector is one of this country’s great industrial success stories — a vital energy supplier, having produced some 43 billion barrels of oil and contributing an enormous £330 billion to the UK economy.

I was in London recently at the IP Week conference and found the conversations really invigorating. What a difference a few months of price stability can have to sentiment. I spoke about, and left feeling even more certain that, we shouldn’t be calling $50 oil a low-price environment.

I was grateful to be invited to address the Aberdeen business community last week as part of the Scottish Council for Development and Industry’s (SCDI) Oil and Gas Industry Leader Series.

While the North Sea is far from being on its last legs, the collapse in the price of oil and the high cost of running ageing infrastructure does mean that production is becoming uneconomic in an increasing number of fields. This has brought decommissioning activity into sharp focus, for upstream producers as well as the supply chain. Similarly, the subject of decommissioning tax relief has attracted much press coverage in recent months.

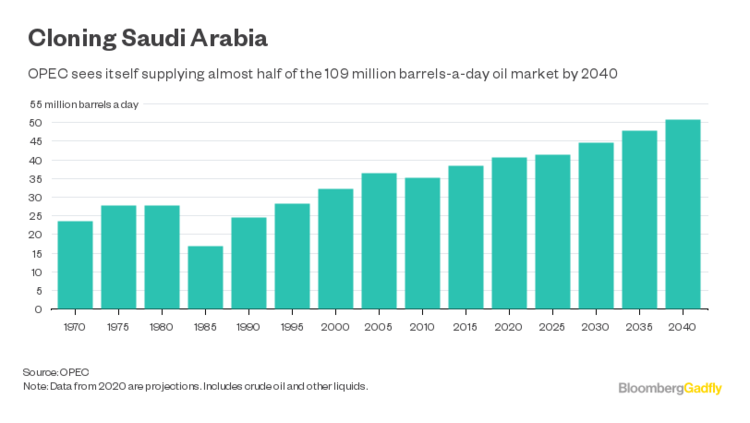

Saudi Arabia has ended up with precisely what it wanted to avoid. Its output cut has left it supporting rival producers, while its sacrifice of volume has yielded little in the way of higher prices. Crude fell back on Thursday to levels not seen since before the producer group announced its historic oil output cuts on Nov. 30. What went wrong, and where do they go from here?

It’s fair to say Philip Hammond’s first (and last) Spring Budget as Chancellor followed the same approach as his first (and last) Autumn Statement – no vote-grabbing gimmicks, no rabbits out of the hat, steady as she goes.

The Budget on March 8, follows hot on the heels of the Autumn Statement on November 23. It is also the first of two Budgets we can expect this year as the UK transitions to an autumn rather than spring budget timetable. Usually it’s only election years during which two Budgets are delivered, but this year is an exception.

Aross literally decades we at the P&J have time and again revisited the relationships between operators, main contractors and the rest of the supply chain.

I’ve played in the Highland League for over 10 years and from my experience of the football transfer system I find the concept of an oil and gas employee loan scheme really appealing.

As an industry we too often have our gaze drawn north towards Aberdeen and south towards London, without giving proper dues to the fantastic work that’s being done in the key energy hubs around the UK.

When I started this campaign to bring decommissioning jobs to Dundee it was the obvious industrial opportunity for our city. Other countries started early to capitalise on the evolution of the North Sea industry. I felt strongly that Dundee, having missed out of industry over the last 40 years, now had a chance to be at the races on this too.