I’m often asked about the role of the OGA, ‘collaboration’, the use of regulatory powers and the impact the authority has made.

The Oil and Gas Authority has been part of the rapidly changing face of the North Sea since 2015. We have a unique role not only to regulate, but to influence change and widely promote all the UKCS has to offer.

In 2016, the OGA became an independent Government Company with a suite of new powers, which we are now actively using in a transparent and targeted manner. I’m pleased the majority of disputes have been resolved without the need for formal sanctions.

Since day one, it’s been a busy, energising and productive time for the authority. We are focused on creating the right conditions, with government support to help the industry succeed amid difficult market conditions. We know how tough it still is, particularly for many in the service sector as the prolonged downturn continues.

Over this period, strong progress has been made by industry with the OGA acting as a catalyst to deliver change – production has increased each year, unit operating costs halved and production efficiency has been steadily rising.

The OGA has worked closely with government to provide incentives with £2.3billion fiscal and £40million seismic packages, making the UKCS a globally competitive region.

Since we started just over two years ago we have added 2.1billion barrels to our forecast despite the prevailing low oil price. As such we are well on track to achieving Sir Ian’s ‘Wood Review’ target of an additional three to four billion barrels.

We are clear on the importance of what we call ‘right assets right hands’. Our work on addressing barriers to investment seems to be working – significant M&A deals have been struck bringing new investment and ideas, demonstrating that companies are seeing the remaining potential of the basin.

We aim to be as transparent as possible. We’ve made huge strides in making comprehensive and quality data available – especially in efforts to reinvigorate our licensing rounds.

In July, the 30th Offshore Licensing Round opened offering acreage in the more mature areas, with some licences available for the first time in 40 years. The Round is being supported by a massive suite of information and data packs to help inform decision makers – this is quite unlike anything that has been done in the past.

It’s a great time to invest with 820 blocks on offer and with the new Innovate Licence creating a more flexible, user-friendly licence for industry.

This round follows the successful 29th Offshore Licensing Round where we awarded 25 licences to 17 companies and the Supplementary Round where 10 companies gained 12 licenses.

With quality data from our new Stewardship Survey, we have been able to publish our Production Efficiency and Decommissioning Cost Estimate Reports. Operators deserve great credit for their positive Production Efficiency results and we expect them to step up again and deliver at least a 35% cost reduction on decommissioning.

Going forward it’s vital that complacency does not set in. Sustaining these hard-fought efficiencies is critical for the North Sea to continue to compete for investment. We at the OGA will continue to do all that we can to help in delivering real value to the oil and gas industry we serve.

We have now identified many billions of additional barrels across the UK Continental Shelf – from the West of Shetland all the way down to the mature Southern North Sea.

Further new ways of working together are needed to maximise the economic recovery.

Rather than talking generically about collaboration we have published specific guidance and expectations – from exploration, stewardship and area plans, all the way through to decommissioning – and supply chain action plans will be coming later this year to assist industry in joining forces.

We will be working closely with leaders on their plans and I need their full support and energy to maximise value from these great opportunities.

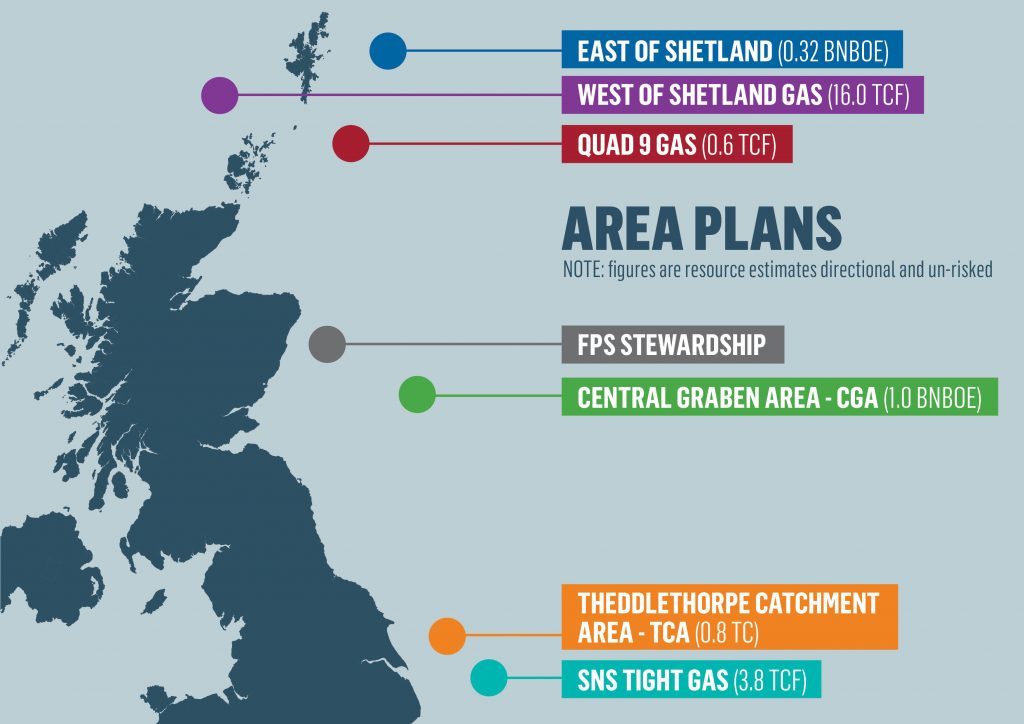

Area Plans are an open invitation for organisations to team up – they involve integrating exploration, development, production, late-life planning and decommission-ing – to ensure the optimum use of infrastructure, to unlock new developments and extend the life of hubs.

Technology is going to be a key part of the MER UK solution and should add substantial further value across the supply chain – including through exports of mature basin solutions. There has been some good work by the Technology Leadership Board and a number of technology organisations over recent years. Being a board member I see first-hand the impressive progress the Oil and Gas Technology Centre is making – we are supporting some really exciting projects. I sense we are fast approaching a positive tipping point as the industry starts to embrace areas such as digital.

I was greatly encouraged by the uptake and energy for the 30th Licensing Round Technology Forum held recently by the OGA and OGTC. It allowed operators, investors and small technology companies to meet and share knowledge to help unlock the UKCS remaining resources, including acreage we are offering in the 30th round.

Going forward we will continue to work in partnership with industry, government and other stakeholders in pursuit of the considerable prize highlighted by Vision 2035.

Delivering MER means making the size of the value ‘pie’ bigger and making a satisfactory return. ‘Collaboration’ is not always an easy path but there are positive incentives and much value to be created by those who want to invest in the UKCS.

Andrew Samuel is chief executive of the Oil and Gas Authority.

Recommended for you