The downturn brought by the Covid-19 pandemic and the accelerating energy transition has created a new reality for the world’s oil and gas industry, whose production will peak lower and earlier than expected before the 2020 market crisis, a Rystad Energy analysis shows.

The five integrated supermajors – ExxonMobil, BP, Shell, Chevron and Total – posted a combined record loss of $76 billion in 2020.

The major chunk of this loss, $69 billion, can be attributed to asset impairments and write-offs as the supermajors re-evaluated their strategy to focus on energy transition and become less dependent on petroleum. Their combined oil and gas output dropped by nearly 5%, or 0.9 million barrels of oil equivalent per day, in 2020 from the year before.

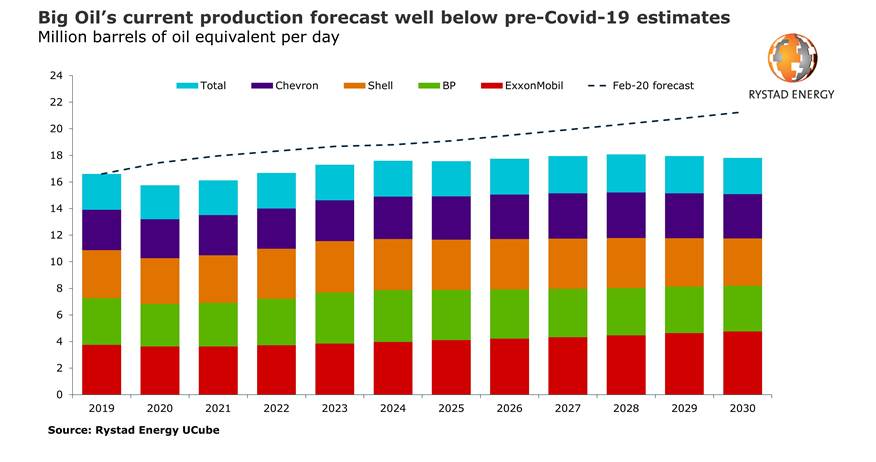

Lower emission targets and demand for cleaner energy have significantly impacted the long-term production outlook for the majors. Rystad Energy forecasts that the majors’ net production will be around 17.5 million boepd in 2025 and peak at around 18 million boepd in 2028, based on our latest revisions. For context, our internal forecast in February 2020 – before the shockwaves from Covid-19 – stood at 19 million boepd for 2025 and 20 million boepd in 2028.

“Last year has certainly tested oil and gas majors like never before. Some recovery can be expected in the near future as demand rebounds and oil prices cross the $60 mark. However, the key to success for the five majors over the next decade will be to strengthen their business in more resilient regions, restructure and resize to match the market needs, and pay back their high debt levels,“ says Rahul Choudhary, upstream analyst at Rystad Energy.

Big oil incurred record loss in 2020, joint output fell by 0.9 million boepd and will peak lower in 2028

The majors’ net income declined sharply last year as low oil prices, OPEC production cuts, collapsing refining margins and weak chemical margins left no business segments unscathed. All the five majors reported net losses in 2020 with ExxonMobil reporting the largest at $22.4 billion, followed by Shell and BP which also incurred losses of more than $20 billion. Total and Chevron fared better than their peers, relatively speaking, as the two companies reported net losses of $5 billion to $6 billion.

Before Covid-19 and the price crash, most companies had assumed an oil price in the range of $70 to $80 per barrel, which allowed them to pursue several higher-cost projects. After the price slump and with continued uncertainty around future oil demand, companies have reduced their price assumptions to between $55 and $70 per barrel, making high-cost projects unviable to pursue.

European majors Shell and BP accounted for the largest year-on-year drop in production with about 300,000 boepd each, while ExxonMobil and Total cut their production by 200,000 boepd and 150,000 boepd, respectively. Chevron was the only major to increase its production in 2020, largely due to its $13 billion acquisition of Noble Energy that partially offset the production curtailments.

At the end of the year, the total spending cuts stood at $26 billion, or 32% of the five majors’ initially announced guidance. Most of the capex cuts relate to greenfield development projects as the majors wait for a recovery in prices and demand before moving ahead with new projects.

Rystad Energy estimates that the five majors approved $30 billion less in greenfield investment in 2020 than they did the year before – a decline of 90%.

US majors ExxonMobil and Chevron raised a record amount of debt during the year, adding $19 billion and $18 billion respectively to their net debt. As a result, both majors increased their gearing ratio by 10% in 2020. While Chevron’s gearing ratio remains below 25%, ExxonMobil’s gearing ratio is now close to 30%, and the company plans to avoid any additional debt in the near future. Due to the heavy debt burdens, both majors had their S&P credit ratings lowered a notch from AA to AA-.

European majors BP and Shell raised their cash in hand by around 50%, thus reducing their overall net debt for the year. However, all of the majors had their gearing ratio raised in 2020, with BP and Shell both ending the year with a gearing above the 30% mark.

Recommended for you