This year could be a turning point for the UK’s onshore unconventional industry.

So far it has been dominated by uncertainty, contradictory resource estimates and, for shale gas, an outright halt to drilling.

But, by the end of 2012, it is hoped the UK Government will have set out its support both for gas as a part of the country’s energy mix and for a resumption of drilling for shale gas.

More clarity is also expected over the level of the UK shale resources, which range from 5.3trillion cu ft to 200trillion cu ft, through new British Geological Society estimates, expected in December.

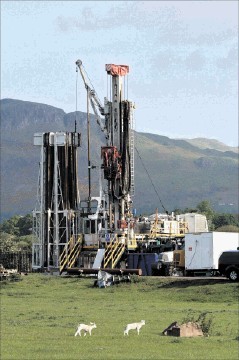

But despite the setbacks, the industry has not been resting on its laurels. While hydraulic fracturing of shale rocks to release gas was halted after a series of minor earthquakes during drilling by Cuadrilla Resources in Lancashire, studies of acreage has continued and commercial coal seam gas production, which does not involve fracking, to the grid is getting closer.

Operators are also working together to form a new industry body, through the joining of the established UK Onshore Oil and Gas Operators Group and newer group, the UK Unconventional Gas Group, aware the industry will need a stronger voice as activity grows.

According to analyst Douglas Westwood, drilling in UK shale could reach 201 wells per year by 2020, with 21 expected in 2013.

However, political support from the coalition government is not yet unanimous. Lib Dem energy secretary Ed Davey described shale gas as “no silver bullet” last month, questioning its potential scale and cost of production.

He is joined by environmental campaigners, WWF and Friends of the Earth, who are concerned about a “dash for gas”, at the cost of renewables, as well as Labour shadow energy minister Tom Greatrex, who has urged caution over predictions of shale gas’ economic potential.

The Conservatives have been more supportive; Chancellor George Osborne suggested introducing a beneficial tax regime for shale gas last month.

New energy minister John Hayes recently said Britain had “great potential” to develop its shale gas fields – once the right regulations are in place.

Dan Byles, a member of the Energy and Climate Change select committee, has also aired his support for shale gas and most recently the Confederation of British Industry backed “safe” shale gas development.

But, even with political support, the industry still faces the challenge of persuading local communities what they are doing is safe.

Graham Dean, managing director of Aberdeen-based Reach Coal Seam Gas, said as well as political support, and clear guidance to local planning authorities, the industry would benefit from having some of the taxes it pays directed straight to the local communities it is working in, rather than any tax incentives.

However, Dean said: “While the ban (on shale fracturing) is in place it is difficult to justify investment. Only when there is confidence that the government wants shale gas will activity accelerate.

“We have delayed our drilling plans to make sure this significant investment is justified.”

While drilling for shale gas has been delayed, the story is more immediately positive for coal seam gas (CSG), or coal bed methane.

Dart International is getting close to CSG commercialisation in Scotland and IGas is expanding its CSG pilot at Doe Green in Cheshire.

CSG is also a target for Reach, which has acreage in the central belt.

“The future is good for coal seam gas,” said Dean. “Both Dart Energy and IGas now have coal seam gas production.

“In the US, coal seam gas production is more than UK North Sea gas production and shale gas in the US is several times larger than North Sea gas production. In the UK, coal seam gas will create an estimated 8,000 to 16,000 jobs.

“The future for shale gas is very good also,” he adds. “Onshore shale gas production in the UK will one day exceed offshore gas production and on the way it will create an estimated 20,000 to 50,000 long-term jobs and pay significant tax revenue and result in a reduction in the country’s greenhouse gas emissions.”